Every January, millions of people on Medicare Part D wake up to find their prescriptions have changed-sometimes without warning. A medication that cost $10 last year now costs $113. A drug you’ve taken for five years is no longer covered at all. This isn’t a mistake. It’s a formulary update, and it’s happening faster and bigger than ever before.

What Exactly Is a Formulary Update?

A formulary is just a list of drugs your insurance plan will pay for. Think of it like a menu at a restaurant: not everything is available, and some items are cheaper than others. Every year, your plan tweaks this menu. In 2025, the changes are more dramatic than ever, thanks to the Inflation Reduction Act (IRA) passed in 2022.These updates aren’t random. They’re driven by cost control. Insurance companies and pharmacy benefit managers (PBMs) like CVS Caremark, OptumRx, and Express Scripts are pushing harder than ever to get patients onto cheaper drugs-especially generics and biosimilars. That’s good news if you’re paying out of pocket. But it’s risky if you’re on a medication that works perfectly for you, and suddenly, your plan says you have to switch.

How the 2025 Changes Hit Your Wallet

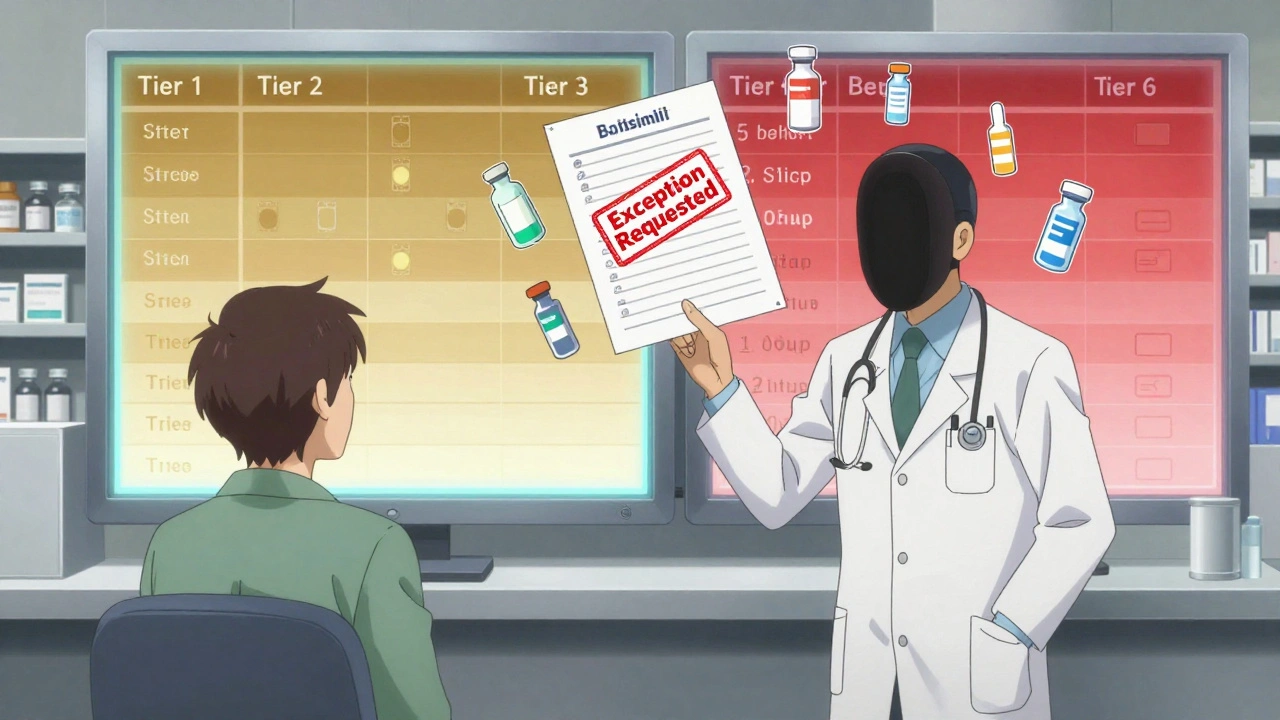

The biggest change in 2025? The $2,000 annual cap on out-of-pocket drug costs. If you spend more than that on prescriptions, your plan pays 100% of the rest. That’s huge. About 3.2 million Medicare beneficiaries will save an average of $1,500 this year, with some saving over $3,000.But here’s the catch: to make that cap work, plans are changing how they structure drug tiers. Here’s what the 2025 tiers look like based on CMS data:

- Tier 1 (Preferred Generics): $1-$10 copay. These are your cheapest options.

- Tier 2 (Non-Preferred Generics & Preferred Brands): Average $47 copay.

- Tier 3 (Non-Preferred Brands): Average $113 copay.

- Specialty Tier: $113 or 25% coinsurance. These are high-cost drugs like biologics.

That $113 price tag? That’s now the standard for many brand-name drugs-even if they’re the only one that works for you. Meanwhile, generics in Tier 1 are almost free. That’s why insurers are pushing hard to move you from a brand to a generic, even if you’ve been stable for years.

Generic Switching: When Your Drug Gets Replaced

Generic switching isn’t new. But in 2025, it’s becoming aggressive. Insurers are removing brand-name drugs from their formularies and replacing them with generics-or even biosimilars, which are like generics for complex biologic drugs.Take Humira, for example. It’s a $7,000-a-year drug used for arthritis and Crohn’s disease. In 2024, its biosimilar Amjevita was approved for full interchangeability. By 2025, many plans are dropping Humira entirely and forcing patients onto Amjevita. One patient on HealthUnlocked reported, “I switched from Humira to Amjevita. Saved $450 a month. No difference in how I feel.”

But not everyone has that luck. Some people report side effects, reduced effectiveness, or just plain anxiety about switching. A 2024 survey found that 23% more patients experienced non-medical switching-changes made by insurers, not doctors-than in 2023. That’s not just a policy shift. It’s a disruption.

What Drugs Are Being Removed?

In October 2024, CVS Caremark announced its 2025 formulary. They removed 16 drugs-nine of them specialty medications. Some of the excluded drugs were Herzuma and Ogivri, two biosimilars that were replaced by newer ones: Kanjinti and Trazimera. Why? Because the newer versions are cheaper and just as effective.UnitedHealthcare moved Humalog insulin to a higher tier, raising copays from $35 to $113 overnight. One Reddit user wrote: “I’ve been on this insulin for 12 years. Now I have to pay three times more. My pharmacist said I could switch to a generic, but my doctor says it’s not safe for me.”

These aren’t isolated cases. In 2025, 78% of standalone Medicare Part D plans (PDPs) are actively pushing for generic substitution. That’s nearly double the rate in Medicare Advantage plans. The reason? PDPs have less flexibility in premiums, so they rely more on drug cost control.

What’s Protected? What’s Not

Not all drugs can be removed. Medicare protects six classes of drugs:- Anticonvulsants

- Antidepressants

- Antineoplastics (cancer drugs)

- Antipsychotics

- Immunosuppressants

- Antiretrovirals (HIV drugs)

If you’re on one of these, your plan can’t drop your drug entirely. But they can still move it to a higher tier. That means higher costs. And they can still require prior authorization or step therapy-forcing you to try cheaper alternatives first.

For example: if you’re on a brand-name diabetes drug, your plan might require you to try metformin or a generic GLP-1 first-even if your doctor says you need the brand. That’s step therapy. And it’s becoming more common.

How to Fight Back: The Exception Process

You don’t have to accept a formulary change. You can request an exception.There are two types:

- Standard Exception: For non-emergency cases. Takes up to 72 hours. Approval rate: 82.3%.

- Expedited Exception: For urgent medical needs. Must be approved within 24 hours. Approval rate: 47.1%.

If your drug was removed entirely, approval is harder. But if it’s just been moved to a higher tier, you have a good shot.

Here’s how to do it:

- Call your doctor. Ask them to write a letter explaining why the generic or biosimilar won’t work for you. Medical necessity is key.

- Submit the request through your plan’s website or phone line. Keep a record of the date, time, and rep you spoke with.

- If denied, file an appeal. You have 60 days to do so.

Cigna’s 2024 data shows 73% of people who requested exceptions got approved. But 38% waited 10 to 14 days for a decision. That’s a long time if you’re running out of meds.

When You Get Notice (And When You Don’t)

By law, insurers must give you 60 days’ notice before changing coverage for a drug you’re already taking. But there’s a loophole: if a new generic is approved, they can change your drug with only 30 days’ notice.That’s why October through December is the most important time of year. That’s when plans release their updated formularies. Don’t wait for a letter. Go online. Check your plan’s website. Download the 2025 formulary PDF. Search your meds. If something’s missing or moved up a tier, act now.

Aetna, for example, gives members a 30-day transitional supply if their drug is being removed. That means you can keep filling your prescription for a month while you work on an exception.

What’s Coming in 2026

2025 is just the warm-up. 2026 is when things get real.The Medicare Drug Price Negotiation Program (MDPNP) kicks in. The government will start negotiating prices for 10 high-cost drugs. The first batch includes Stelara, Prolia, and Xolair. Starting January 1, 2026, every Part D plan must cover these drugs-at the negotiated price.

That’s a game-changer. It means biosimilars for these drugs will flood the market. And insurers will push them even harder. By 2026, 65% of plans are expected to require generic or biosimilar substitution for non-protected drugs.

And it’s not just Medicare. Private insurers are watching closely. If the government can force down prices on these drugs, they’ll follow suit.

What You Should Do Right Now

It’s December 2025. You don’t have much time left. Here’s your action plan:- Check your formulary. Log into your plan’s website. Search every drug you take.

- Call your pharmacist. They see formulary changes every day. Ask: “Is my drug staying on the list? Is there a cheaper alternative?”

- Talk to your doctor. If your drug is being removed or moved, ask: “Can we switch now, before January 1? Or should I file an exception?”

- Don’t wait for a letter. If your drug is gone on January 1, you’ll be stuck paying full price for weeks.

- Know your rights. You can appeal. You can get a 30-day supply. You can ask for an emergency exception.

Generic switching isn’t evil. It’s smart economics. Biosimilars save billions. But for people with chronic conditions, it can feel like a gamble. Your health shouldn’t be a cost-cutting experiment. If your medication works, fight to keep it. Use the tools you have. Demand better communication. And never assume your plan has your back-check for yourself.

What’s Next?

The trend won’t stop. More drugs will become generics. More biosimilars will enter the market. More plans will push for substitution. The goal is lower costs. But the human cost? That’s up to you to protect.What happens if my drug is removed from the formulary?

If your drug is removed, you’ll get a notice at least 30 days before the change. You can request an exception through your plan. If approved, you’ll keep your drug at the same cost. If denied, you can appeal. In the meantime, your plan must give you a 30-day transitional supply so you don’t run out.

Can I switch to a biosimilar even if my doctor doesn’t recommend it?

Yes, your plan can require you to switch to a biosimilar-even if your doctor hasn’t approved it. But you can file an exception if you have a medical reason to stay on your current drug. The FDA allows biosimilars to be used without being labeled "interchangeable," as long as they’re proven safe and effective. Still, if you’ve had issues with previous switches, your doctor’s note is your best tool.

Why are some drugs cheaper than others even if they’re the same?

It’s about tier placement. Generic versions of the same drug can be placed on different tiers based on what your plan negotiates with manufacturers. One generic might be in Tier 1 ($10), another in Tier 2 ($47), even if they’re chemically identical. That’s because the plan gets a bigger discount from one manufacturer. Your pharmacist can tell you which generic version your plan prefers.

How do I know if a biosimilar is right for me?

Biosimilars are highly similar to their brand-name counterparts and have been tested for safety and effectiveness. Many patients switch without issue. But if you’ve had allergic reactions, immune responses, or inconsistent results with previous switches, talk to your doctor. Monitor your symptoms closely for the first 3-6 months after switching. Keep a journal. If you feel worse, report it immediately.

Can I switch plans to avoid formulary changes?

You can only switch Medicare Part D plans during the Annual Enrollment Period (October 15-December 7). If you missed it, you can’t switch until next year-unless you qualify for a Special Enrollment Period (like moving to a new state or losing other coverage). Don’t wait until January to realize your drug is gone. Check your formulary now.

Are there any drugs that can’t be switched at all?

Yes. Medicare protects six drug classes: anticonvulsants, antidepressants, antineoplastics, antipsychotics, immunosuppressants, and antiretrovirals. Plans can’t remove these entirely. But they can still move them to higher tiers or require prior authorization. So even protected drugs aren’t always safe from cost increases.

What if I can’t afford my drug after a formulary change?

You have options. First, ask your doctor about patient assistance programs. Many drugmakers offer free or low-cost drugs to people who qualify. Second, check with local pharmacies-some offer cash discounts on generics that beat insurance prices. Third, contact your State Health Insurance Assistance Program (SHIP). They offer free counseling on Medicare and drug coverage.

12 Comments

nithin Kuntumadugu

December 14, 2025 AT 02:18lol so now the gov't is gonna force us all onto cheap meds like we're lab rats? 🤡 next they'll be putting fluoride in our insulin. they don't care if you die, they just want to save $2.00 per pill. #BigPharmaIsWatching

John Fred

December 14, 2025 AT 07:05Hey everyone - big picture here: the $2K cap is a GAME CHANGER. 🚀 Even if you get switched to a generic, you're still saving hundreds monthly. And biosimilars? They're FDA-approved clones - not some sketchy knockoff. Talk to your doc, sure - but don't panic. This is progress, not punishment. 💪

Cole Newman

December 14, 2025 AT 09:39You guys are acting like switching from Humira to Amjevita is like swapping your kidney. It's the same protein, same mechanism, same clinical trials. If your doctor says 'it's not safe' but you've been stable for 5 years, maybe your doc is just scared of change. I switched last year. Zero side effects. Save your cash.

Casey Mellish

December 15, 2025 AT 20:44Australia's been doing this for years - generics are the norm, and we've got one of the best healthcare systems on earth. The key is transparency and support. If your plan forces a switch, they should also fund a 3-month follow-up with your specialist. No one should be left in the dark. 🇦🇺

Tyrone Marshall

December 16, 2025 AT 23:06Let’s not villainize cost control. The system is broken because we let drug prices balloon for decades. Generics aren’t the enemy - greed is. But I get it: when you’ve found a drug that works, it’s terrifying to be told you have to change. The real issue? Lack of communication. If your plan drops your med, they owe you more than a PDF. They owe you a conversation.

Emily Haworth

December 17, 2025 AT 14:52Wait… so if they can switch me to a biosimilar, what’s stopping them from switching me to a *placebo* next year? 😳 I’ve seen too many people get worse after these switches. This isn’t economics - it’s medical roulette. And who’s betting? The CEOs. Who’s losing? Us.

Himmat Singh

December 17, 2025 AT 15:26It is imperative to note that the regulatory framework governing pharmaceutical formularies is predicated upon actuarial equity and fiscal sustainability. The transition to biosimilars is not capricious; it is an evidence-based imperative aligned with global best practices. To conflate cost containment with malfeasance is to misunderstand the architecture of public health financing.

Alvin Montanez

December 18, 2025 AT 09:49You think this is bad? Wait till you see the 2026 list. The government is negotiating prices for Stelara and Xolair - which means those drugs are gonna be forced onto EVERYONE. Even if you’re allergic. Even if your body screams no. They’re not asking. They’re telling. And if you don’t like it? Tough. You’re not special. You’re a line item.

Lara Tobin

December 19, 2025 AT 00:58I just lost my dad to a switch that went wrong. He was on a brand-name drug for 10 years. They moved him to a generic. He got worse. They said it was 'just adaptation.' He didn't adapt. He died. I'm not mad at the system. I'm just… tired. Please, if you're switching - monitor. Journal. Speak up. Don't let anyone tell you it's 'just a pill.'

Jamie Clark

December 20, 2025 AT 01:28You’re all missing the point. The real villain isn’t the insurer, it’s the FDA. They approved these biosimilars as 'interchangeable' without real-world, long-term data on immune response. You think a 3-month study proves safety for someone with Crohn’s on Humira for 15 years? That’s not science. That’s corporate lobbying dressed in a lab coat.

Keasha Trawick

December 21, 2025 AT 16:19Okay but imagine if your Netflix show got replaced with a knockoff version because it was cheaper. You’d be PISSED. Same thing here. That drug you’ve been on? It’s your personal Netflix. They didn’t ask. They just swapped it for a 720p version and called it 'HD.' And now you’re supposed to be grateful? 🤦♀️

Deborah Andrich

December 22, 2025 AT 03:43I’m not here to fight. I’m here to help. If your drug got pulled, call your SHIP counselor. They’re free. They’ll walk you through the exception form. I’ve helped 12 people this month. You’re not alone. And if you’re scared? Say it out loud. We’ve all been there. This isn’t about being right. It’s about being heard.